An Awkward Fit for Jobs Impacts in Benefit-Cost Analysis

Synapse recently tackled an interesting challenge while analyzing a community solar program and its alternatives on behalf of the Rhode Island Division of Public Utilities and Carriers: Where do jobs and other macroeconomic impacts fit into a good benefit-cost analysis (BCA)?

Rhode Island’s Public Utilities Commission (PUC) requires that utility spending proposals be supported by a BCA, and these BCAs in turn must be based upon the Rhode Island benefit-cost test (RI Test). In practice, this means that potential investments are judged by their impacts both within the utility system and beyond. The RI Test accounts for various non-utility impacts, including impacts on the environment and economy.

The emphasis on BCA and the wide perspective of the RI Test makes good economic sense but implementing these requirements can be nuanced. On the surface, the PUC’s prior guidance to decision-makers about macroeconomic impacts and BCAs seems clear enough: when comparing two alternative utility investment plans, all else equal, the one with superior macroeconomic impacts should be chosen. In practice, this issue is often more complicated.

While we relied on existing precedent for guidance in accounting for environmental and public health impacts, we still needed to determine how to account for macroeconomic impacts in our analysis.

Should macroeconomic impacts be added to other costs and benefits in the BCA?

BCAs often consider a wide array of different impacts. Those impacts that can be expressed in monetary terms (monetized) are usually added up to produce one or more top-line results—in particular, the project’s net benefits and its benefit-cost ratio (BCR).

On the other hand, impacts that cannot be monetized must by necessity be reported separately. Since macroeconomic effects can be monetized—in terms of changes in GDP, income, or other impacts—it’s easy to assume that they should be added into the net benefits or BCR. The Synapse team, however, concluded that this assumption would likely result in inaccurate total impacts.

After considerable internal debate and consulting with leading practitioners in the field, we concluded that adding monetized macroeconomic impacts into BCA results could result in double-counting of costs and/or benefits that might contribute to a distorted view of overall project impacts.

The core concern is that nearly identical values enter into both the BCA and the economic impact analysis. In the context of a renewable energy program, examples of these repeated values are:

- Reductions in utility-system spending on traditional resources: In the BCA, these appear as avoided costs, which is a positive outcome. In the economic impact analysis, the same reduction in spending leads to reduced economic activity, which is a negative outcome.

- Increases in spending on new resources: In the BCA, increased spending on new resources (such as photovoltaic solar) appears as a cost, which is a negative outcome. In the economic impact analysis, this increase in spending leads to increased economic activity, which is a positive outcome.

- Customer bill impacts: These are the differences between the utility system benefits and costs, and they may be either a net benefit or a net cost in a BCA. Similarly, the bill impacts may result in either an increase or a decrease in economic activity in the economic impact analysis. However, unlike the two effects described above, favorable bill impacts in the BCA result in increased economic activity in the economic impact analysis. That is, these effects are in the same direction rather than offsetting.

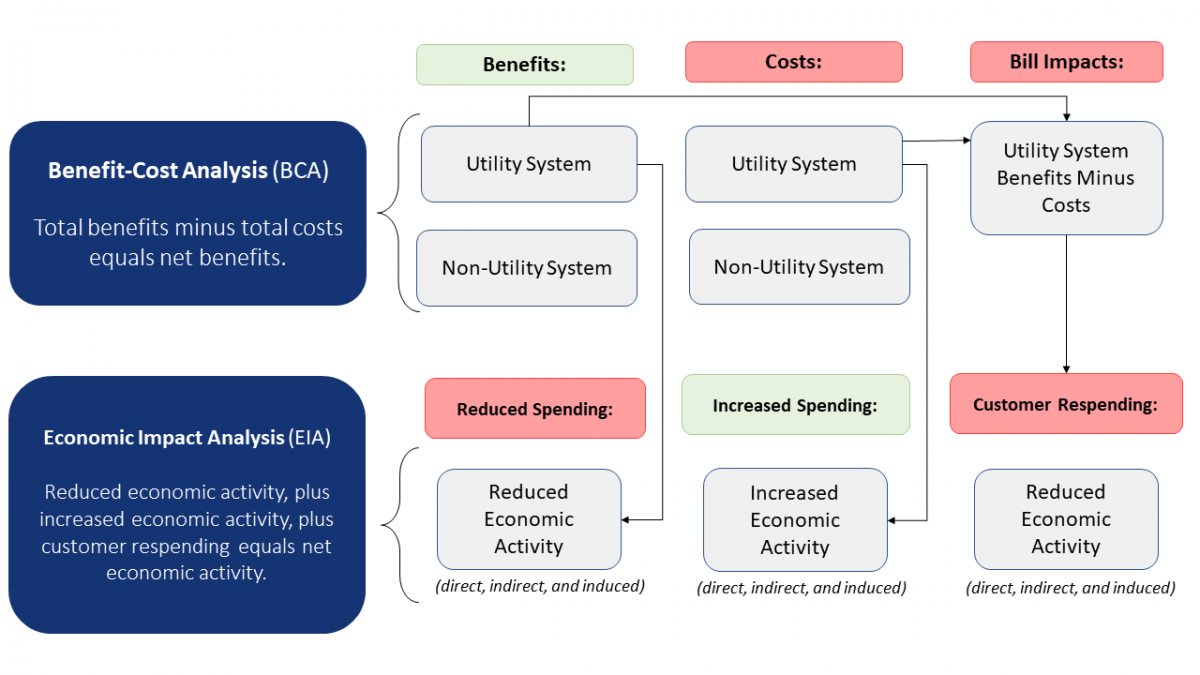

Comparison of benefit-cost analyses and economic impact analyses

The figure below illustrates the overlap between BCA and economic impact analysis evaluations. In this example, a renewable energy proposal is subject to review using both BCA and economic impact analysis. The project in question is expected to result in a net increase in customer bills, which in turn will reduce economic activity.

There is at least one other, more pragmatic reason not to add macroeconomic impacts into BCA results. If macroeconomic impacts were to be added directly into costs and benefits in the BCA, then it would be necessary to choose which macroeconomic indicator to use. Adding multiple indicators into the results would surely overstate impacts. Yet none of the macroeconomic indicators tells the complete story.

GDP can be blunt or misleading. Jobs and income impacts are more tangible. But jobs cannot be monetized (and so cannot be added directly to monetized benefits and costs) and income in isolation provides too limited a view.

While the PUC has not provided explicit direction on which macroeconomic measures should be reported in conjunction with a BCA, the Synapse team reached a simple conclusion:

BCAs under the RI Test should report all of the economic impact analysis indicators, including GDP, income, and jobs impacts—and none of these indicators should be added to the monetary results of the BCA.