AEO 2026 shows the growing importance of electricity affordability across the economy

On April 8, 2026, the U.S. Energy Information Administration (EIA) released the 2026 Annual Energy Outlook (AEO). AEO 2026 contains projections of energy use and energy prices for the electric power, residential, commercial, industrial, and transportation sectors through 2050. The 2026 report’s Counterfactual Baseline case (formerly called the Reference case) is a projection of the future U.S. energy system based on EIA estimates of fuel availability, changes in technology costs, and current legislation. This Counterfactual Baseline (CB) includes implementation of April 2024 revisions to Section 111 of the Clean Air Act, which regulates carbon dioxide (CO2) emissions from fossil fuel generating units. Because the U.S. Environmental Protection Agency (EPA) proposed to repeal this rule in June 2025, EIA also models an Alternative Electricity (AE) case without Section 111 regulations of fossil fuel generation. Given the uncertainty in implementation of the 111 rule, we compare these two policy cases throughout this blog post.

Compared to previous AEO forecasts, AEO 2026 projects dramatically higher electricity prices across the residential, commercial, and industrial sectors, highlighting the growing importance of energy affordability to U.S. energy consumers. In terms of emissions, AEO 2026 shows that electricity sector emissions will decline but are still miles from being carbon-free. In fact, the AEO now projects an increase in electric sector CO2 emissions after 2040. Further action will be needed to decarbonize the sector and mitigate climate impacts, though doing so will require balancing emissions reductions with rising affordability pressures, as fuel price dynamics, changing policies, and higher system demand and associated costs increasingly affect electricity prices for consumers.

AEO 2026 revises projected electricity prices upwards for all sectors

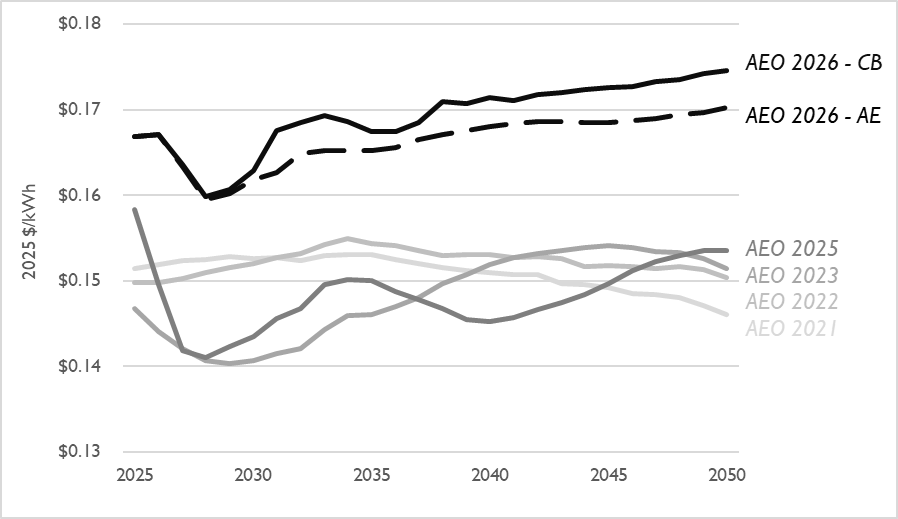

AEO 2026 represents a large jump in projected electricity prices for the residential, commercial, and industrial sectors over prior projections. In the residential sector, the AEO 2026 Counterfactual Baseline projects an average retail electricity price for U.S. residential electricity consumers of $0.17 per kWh in 2026, up from the $0.15 per kWh projection made by AEO 2025, or an increase of 12 percent (see Figure 1). These upward projections reflect the observed real increases in electricity prices across the country. We hypothesize that this jump in projected electricity prices in AEO 2026 is driven by factors such as electricity demand growth, new policies in 2025, and upward natural gas price trajectories. In fact, AEO documentation notes that natural gas prices and electricity prices are tightly correlated. AEO 2026 has a higher natural gas price trajectory for residential consumers relative to AEO 2025, indicating overall increases in energy prices for residential consumers. Across sectors, the jump in projected electricity prices from AEO 2025 to AEO 2026 was steepest for the residential sector, though also present for the commercial and industrial sectors.

Under the Alternative Electricity case without implementation of revised Section 111 rules, projected increases in electricity prices from 2030 onwards are slightly dampened compared to the Counterfactual Baseline case. We hypothesize that this is because the Alternative Electricity case does not require carbon capture and sequestration (CCS) technology for fossil generation, which can be costly to retrofit. Still, even without Section 111 rules, AEO 2026 Alternative Electricity prices are higher than previous AEO estimates, driven in large part by higher projections of natural gas hub prices (see Figure 5, below).

Figure 1. Comparison of residential electricity price projections across AEO 2026 cases and prior AEO Reference cases

Note: y-axis does not start at zero

Current policies will not achieve a carbon-free electric sector, and AEO 2026 even projects an uptick in electric sector CO2 emissions after 2040

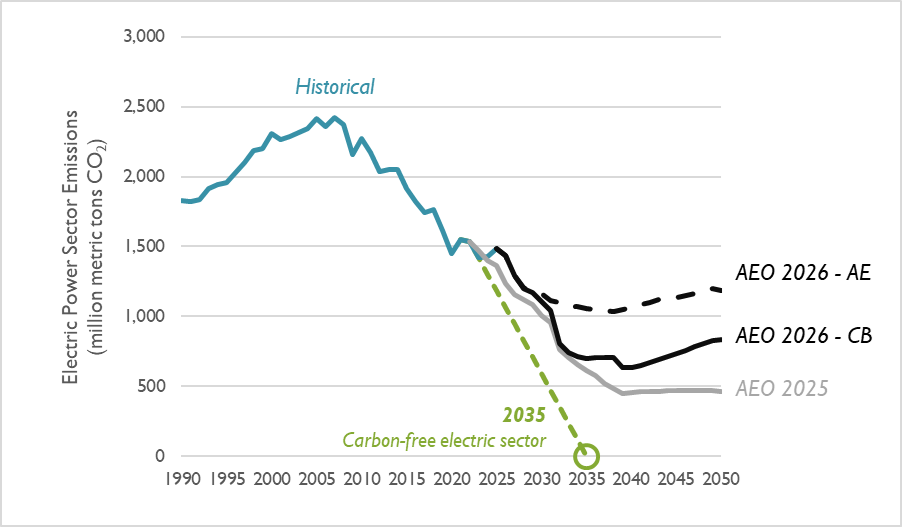

AEO 2026 shows electric sector carbon dioxide (CO2) emissions will largely decline through 2040; however, from there, emissions plateau and actually increase (Figure 2). Under the Counterfactual Baseline case, electric sector CO2 emissions increase after 2040 because AEO 2026 projects that under this case, CCS deployment declines as incentives like the 45Q tax credit expire, reducing the amount of CO₂ captured from fossil fuel plants. At the same time, the Counterfactual Baseline case in AEO 2026 projects that natural gas generation remains economically competitive in the longer term, so fossil fuel use persists without CCS. This combination leads to the reverse in declining emissions. For the Alternative Electricity case without Section 111 CO2 emissions regulations for fossil generation, emissions do not drop as much as in the Counterfactual Baseline case.

The previous administration had a stated goal of achieving a carbon-free electric sector by 2035. While multiple states have carbon-free commitments in various forms and timelines, AEO 2026 shows that the U.S. electricity sector is not on track to meet these goals in either the medium or long term without additional policies.

Figure 2. Comparison of electric-sector CO2 emission projections in the AEO 2025 and AEO 2026 Reference cases (called Counterfactual Baseline case in AEO 2026)

Increased projected electricity demand in AEO 2026 relative to AEO 2025 is primarily met by natural gas generation

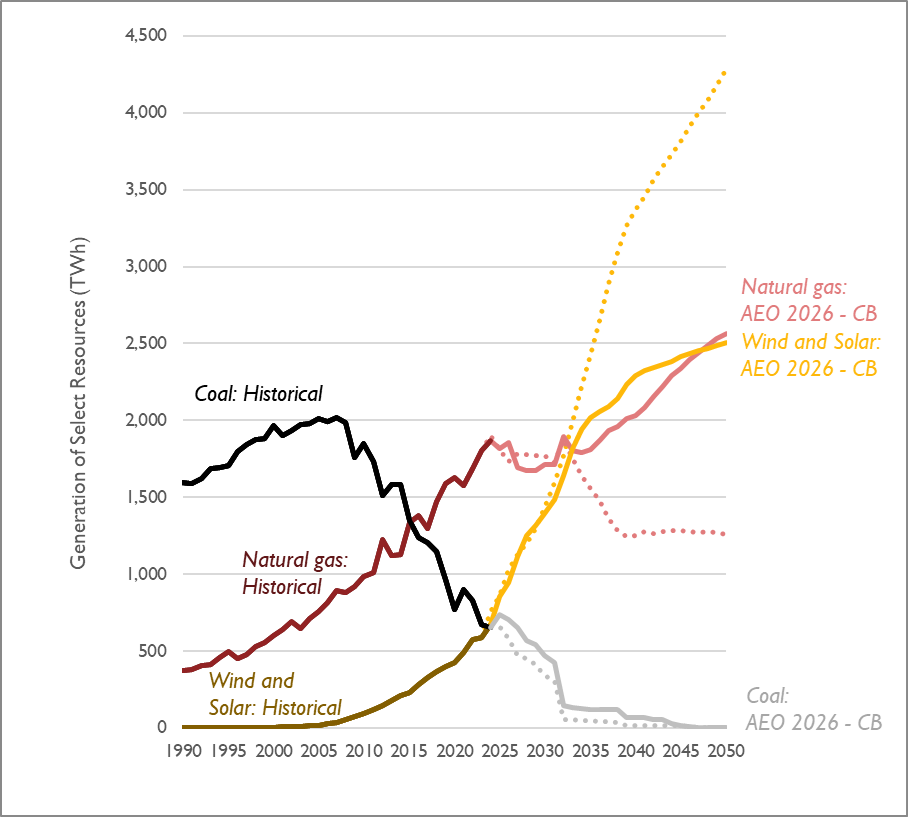

The AEO 2025 Reference case projected that wind and solar generation would outstrip natural gas generation before the end of this decade, and by 2050, make up more than double the amount of natural gas–based electricity generation. However, AEO 2026 projects a future electricity generation mix with lower amounts of wind and solar and more natural gas, with the combined generation share of these technologies reaching 80 percent by 2050. Overall electricity demand projections increased in AEO 2026, with higher growth rates relative to AEO 2025 driven in large part by data center server energy use. AEO 2026 projects that natural gas electricity generation will increase to meet this demand.

- Wind and solar: Like AEO 2025, AEO 2026 projects a ramp up of solar and wind through the rest of the decade. However, the longer-term trajectory for these resources tapers off relative to AEO 2025 due to a phaseout of incentives and changes in cost-competitiveness between these resources and natural gas (see Figure 3). Wind and solar generation reach about 2,500 TWh in 2050.

- Natural gas: EIA notes that its projections are very sensitive to natural gas prices and technology costs due to tight cost competition between natural gas and wind and solar. Under the Counterfactual Baseline, updated cost and policy assumptions tilt the economics toward natural gas over renewables. The Counterfactual Baseline also assumes that the Section 111 rule is in place , limiting new natural gas turbines to a maximum 40 percent annual capacity factor. This actually increases overall installed natural gas capacity and generation.

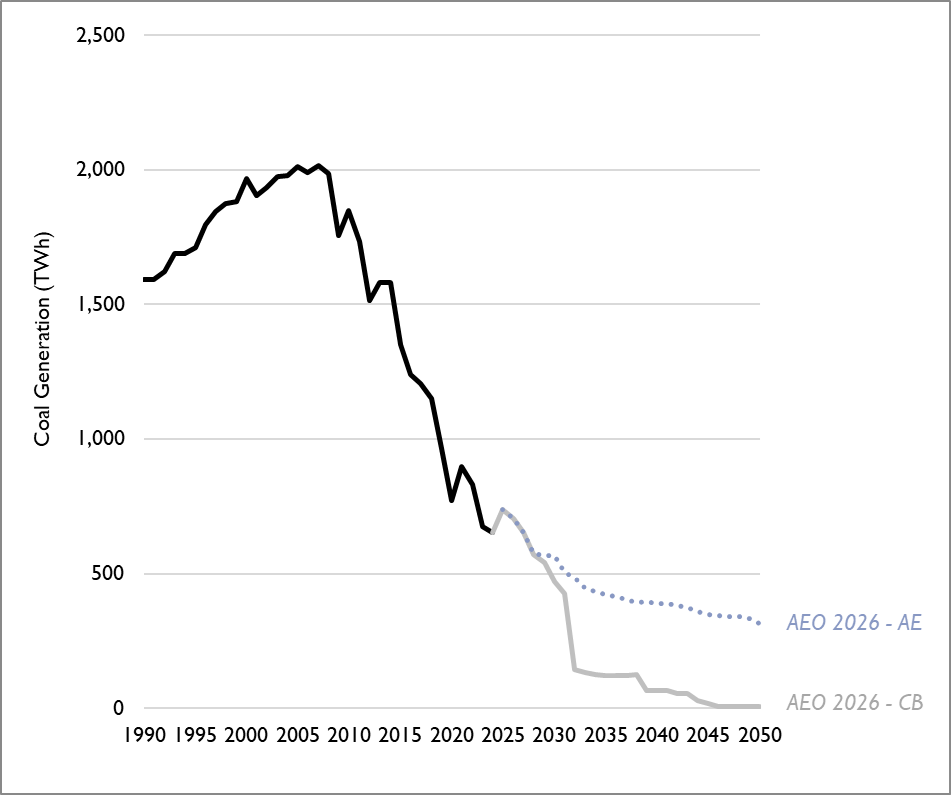

- Coal: EIA projects that coal-fueled generation will decline steeply due to the 111 rule. This retirement of coal is accompanied by an increase in natural gas combustion turbine capacity. Even under the Alternative Electricity case without the 111 rule, EIA is projecting that coal generation continues to decrease (see Figure 4), representing just 5 percent of electricity generation by 2050.

Figure 3. Comparison of electricity generation from coal, natural gas, and wind and solar in the AEO 2026 Counterfactual Baseline and AEO 2025 Reference case (series from AEO 2025 are shown as dotted lines)

Note: This figure does not include generation from hydro, nuclear, geothermal, biomass, and miscellaneous sources.

Figure 4. Comparison of coal generation under the AEO 2026 Counterfactual Baseline case (with 111 rule) and the Alternative Electricity case (no 111 rule)

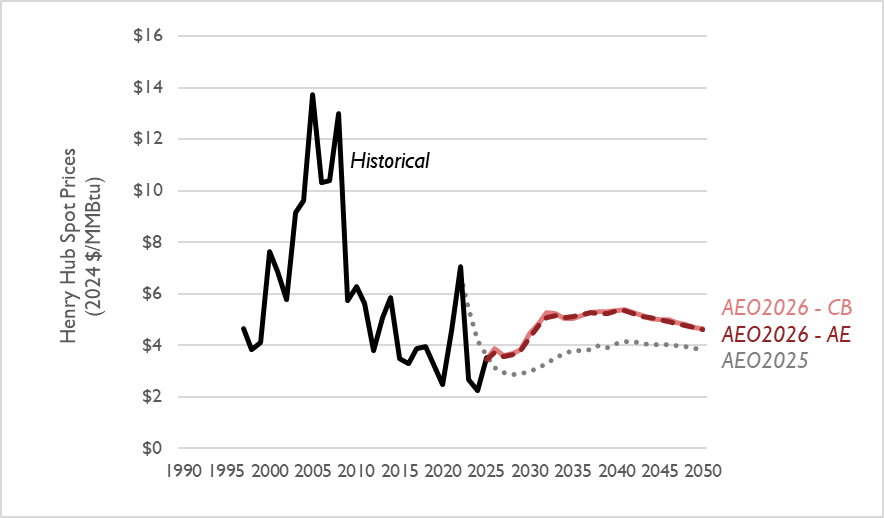

The resource mix across wind, solar, natural gas, and coal generation is driven in part by the dynamics of the latest AEO’s natural gas price projection (see Figure 5). AEO 2026 reflects the near-historically low natural gas prices experienced in 2024 and the increase observed in 2025. However, AEO 2026 has an overall higher trajectory for natural gas prices than AEO 2025. Henry Hub natural gas prices are projected to rise from 2027 through 2032 due to growing liquified natural gas (LNG) exports and domestic demand, especially from the power and industrial sectors. After 2040, prices decrease as supply growth paces demand. Higher natural gas price projections trickle across the economy, also driving AEO 2026’s higher electricity price projections (see Figure 1).

Projected Henry Hub prices are very similar across the Counterfactual Baseline and Alternative Electricity cases in AEO 2026 (see Figure 5). In fact, Henry Hub price trajectories are very similar across all AEO 2026 cases, except for the High Oil and Gas Supply and Low Oil and Gas Supply cases (not pictured), which set much lower and higher bounds on Henry Hub prices, respectively.

Figure 5. Comparison of natural gas prices at the Henry Hub in the AEO 2026 Counterfactual Baseline and Alternative Electricity cases vs. the AEO 2025 Reference case

Future load from data centers remains high in AEO 2026, while transport electrification is highly policy dependent

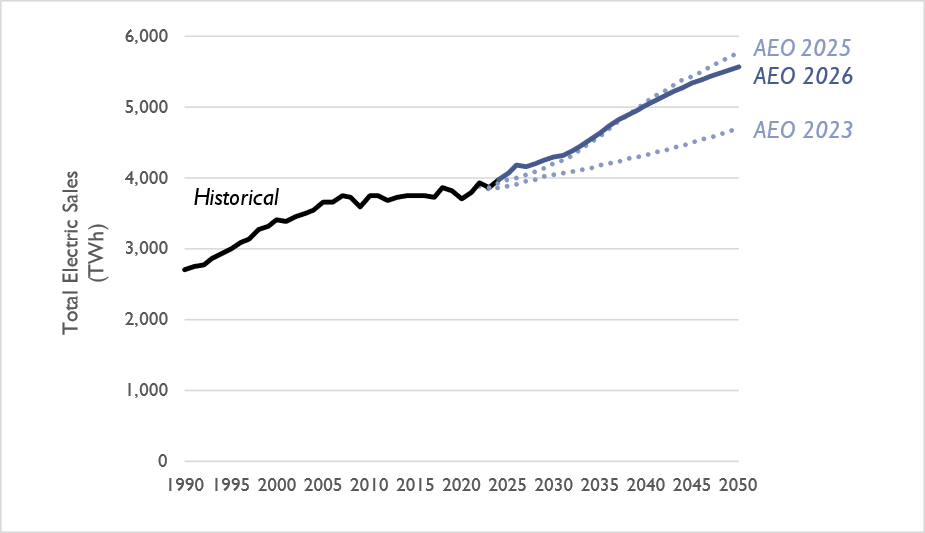

Aggregated electricity generation from coal, natural gas, renewables, and other resources in AEO 2026 and AEO 2025 are much higher compared to the previous AEO projection before that, AEO 2023 (see Figure 6). Like AEO 2025, AEO 2026 incorporates increases in projected load from data centers and electrification (particularly electric vehicles), with data centers making the commercial sector the highest and fastest-growing electricity-consuming sector. EIA notes that it now breaks out data center server energy use from other commercial computing end use, and uses power draw and installed stock data to make these estimates. To reflect uncertainty in future computing demand and efficiency, EIA also models a High Electricity Demand case (not pictured below), wherein data centers account for all incremental electricity demand growth and data center server electricity consumption in 2050 is more than 16 times that in 2020.

Figure 6. Comparison of electricity sales projections in the AEO 2026 Counterfactual Baseline and AEO 2023 and 2025 Reference cases

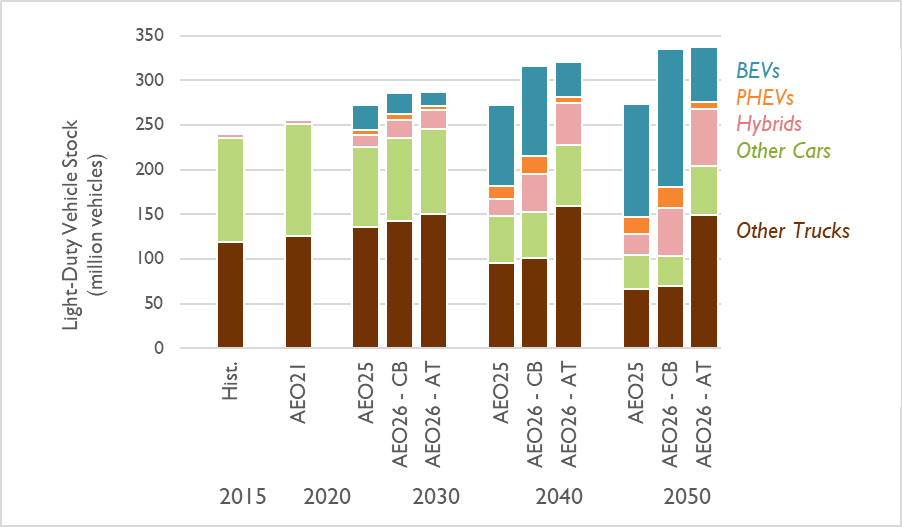

The AEO 2026 Counterfactual Baseline case projects higher growth across vehicle categories, especially hybrid vehicles, compared to AEO 2025’s reference case. The Counterfactual Baseline includes EPA’s vehicle tailpipe emission standards for model years after 2027. However, to understand the potential impact of removing these standards, EIA also modeled an Alternative Transportation case without these standards and with subsequent adjustments to vehicle manufacturing growth and charging infrastructure buildout. Under the Alternative Transportation case, battery electric vehicles (BEVs) make up a much smaller share of light-duty vehicle stock by 2050 compared to the Counterfactual Baseline that has standards in place, demonstrating the important role of regulation in driving electric vehicle adoption and manufacturing decisions.

Figure 7. Light-duty vehicle stock in the AEO 2025 Reference case and AEO 2026 Counterfactual Baseline (CB) and Alternative Transportation (AT) cases

Note: BEVs includes all-electric vehicles. PHEVs includes plug-in hybrids, while Hybrids constitute non-plug-in hybrids. All other alternative light-duty vehicles are included in Other Cars and Other Trucks.